One of the best investments we can make is in our own knowledge and skill set. With that in mind, this article will work through how we can use Return On Equity (ROE) to better understand a business. To keep the lesson grounded in practicality, we’ll use ROE to better understand Centum Electronics Limited (NSE:CENTUM).

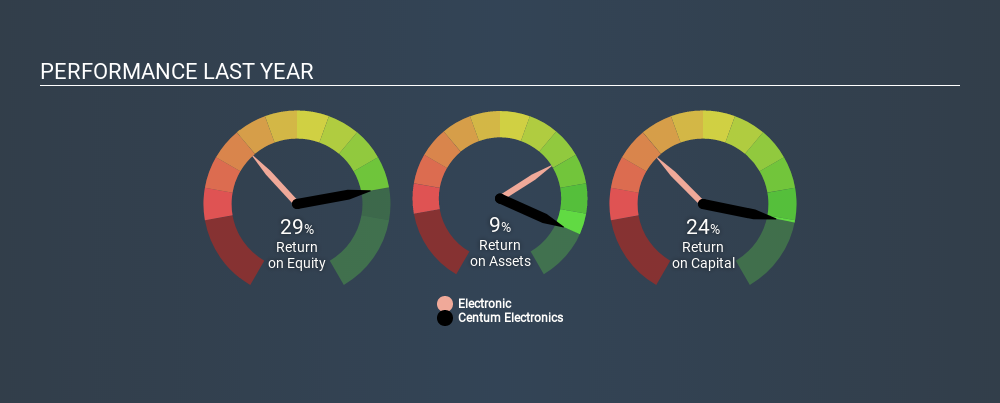

Centum Electronics has a ROE of 29%, based on the last twelve months. That means that for every ₹1 worth of shareholders’ equity, it generated ₹0.29 in profit.

See our latest analysis for Centum Electronics

How Do I Calculate Return On Equity?

The formula for return on equity is:

Return on Equity = Net Profit ÷ Shareholders’ Equity

Or for Centum Electronics:

29% = ₹728m ÷ ₹2.5b (Based on the trailing twelve months to September 2019.)

It’s easy to understand the ‘net profit’ part of that equation, but ‘shareholders’ equity’ requires further explanation. It is all the money paid into the company from shareholders, plus any earnings retained. Shareholders’ equity can be calculated by subtracting the total liabilities of the company from the total assets of the company.

What Does ROE Signify?

ROE measures a company’s profitability against the profit it retains, and any outside investments. The ‘return’ is the profit over the last twelve months. That means that the higher the ROE, the more profitable the company is. So, all else equal, investors should like a high ROE. Clearly, then, one can use ROE to compare different companies.

Does Centum Electronics Have A Good Return On Equity?

By comparing a company’s ROE with its industry average, we can get a quick measure of how good it is. However, this method is only useful as a rough check, because companies do differ quite a bit within the same industry classification. Pleasingly, Centum Electronics has a superior ROE than the average (9.2%) company in the Electronic industry.

That’s clearly a positive. We think a high ROE, alone, is usually enough to justify further research into a company. One data point to check is if insiders have bought shares recently.

How Does Debt Impact ROE?

Companies usually need to invest money to grow their profits. That cash can come from retained earnings, issuing new shares (equity), or debt. In the case of the first and second options, the ROE will reflect this use of cash, for growth. In the latter case, the debt required for growth will boost returns, but will not impact the shareholders’ equity. That will make the ROE look better than if no debt was used.

Centum Electronics’s Debt And Its 29% ROE

Centum Electronics clearly uses a significant amount of debt to boost returns, as it has a debt to equity ratio of 1.05. There’s no doubt its ROE is impressive, but the company appears to use its debt to boost that metric. Investors should think carefully about how a company might perform if it was unable to borrow so easily, because credit markets do change over time.

In Summary

Return on equity is a useful indicator of the ability of a business to generate profits and return them to shareholders. A company that can achieve a high return on equity without debt could be considered a high quality business. If two companies have the same ROE, then I would generally prefer the one with less debt.

Having said that, while ROE is a useful indicator of business quality, you’ll have to look at a whole range of factors to determine the right price to buy a stock. The rate at which profits are likely to grow, relative to the expectations of profit growth reflected in the current price, must be considered, too. You can see how the company has grow in the past by looking at this FREE detailed graph of past earnings, revenue and cash flow.

Of course Centum Electronics may not be the best stock to buy. So you may wish to see this free collection of other companies that have high ROE and low debt.

[“source=simplywall”]